RevPAR, revenue per available room, is the single metric most hotel ownership groups and asset managers use to benchmark property performance. It captures rate and occupancy together in one number, making it easy to compare across properties and competitive sets. What it does not capture is where that revenue is coming from.

For hotels with meaningful group and corporate business, group contribution to RevPAR tells only part of the story. The group segment’s contribution to total revenue is often underestimated when evaluated through a room-rate lens alone, and revenue managers who price against a transient-only model are routinely making displacement decisions with incomplete information.

This guide explains how group business actually contributes to RevPAR and total hotel revenue, why group ADR comparisons to transient ADR are the wrong measurement, and what revenue managers need from the sales team to evaluate group contribution accurately.

What RevPAR Measures — and What It Misses

RevPAR is calculated by multiplying average daily rate (ADR) by occupancy, or by dividing total room revenue by available rooms. It is a room revenue metric. It does not include food and beverage revenue, meeting room rental, AV charges, spa, parking, or any other ancillary revenue stream.

For a limited-service hotel where room revenue is nearly all the revenue, RevPAR is a reasonable proxy for total performance. For a full-service or upper-upscale hotel where group business drives significant F&B and event revenue, RevPAR on its own is structurally incomplete as a performance measure.

The implication for group business specifically: a group booking that appears to underperform on room rate may actually generate strong total revenue contribution once all revenue streams are included. Evaluating it solely on room ADR versus transient ADR produces the wrong answer, sometimes by a wide margin.

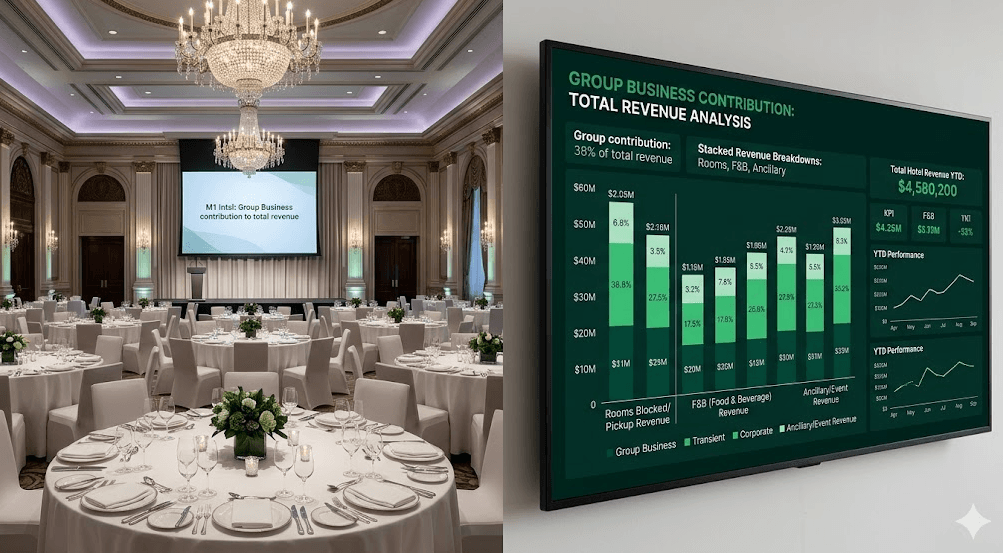

How Group Business Contributes to Total Hotel Revenue

Group business contributes to hotel revenue across multiple streams simultaneously, which is what makes room-rate-only comparisons misleading.

Room revenue

Group room blocks are contracted at negotiated rates, often with attrition and cancellation clauses that provide revenue protection even if the group doesn’t fully actualize. The room rate is typically below peak transient rate, but it provides a reliable, forecasted revenue base that transient business cannot match in terms of certainty. Group room revenue on the books months in advance is what allows revenue managers to price remaining transient inventory with confidence.

Food and beverage

For full-service hotels, group F&B is frequently the highest-margin revenue stream attached to a group booking. Meeting packages, banquet dinners, breakfast events, coffee breaks, and reception bars all carry contribution margins that can equal or exceed the room revenue from the same group. A corporate meeting for 80 attendees over two days may generate as much in F&B revenue as it does in room revenue, sometimes more.

Meeting room and event space rental

Groups that use meeting rooms, ballrooms, or breakout spaces generate rental revenue that is separate from room and F&B. For properties with significant event infrastructure, this is a meaningful revenue stream that does not appear in any RevPAR calculation.

Ancillary spend

Group attendees typically spend more on property than comparable transient guests. Capture rates for restaurant dining, spa, fitness, parking, and resort amenities are consistently higher among attendees on property for a multi-day program. The incremental ancillary revenue from a group booking is real, and rarely factored into displacement analysis at most properties.

The room rate comparison is the wrong question

Asking whether group ADR is above or below transient ADR misses the point. The right question is whether total group revenue contribution (rooms plus F&B plus ancillary plus attrition protection) exceeds the total transient value of the same room nights. That comparison requires data the sales team must provide before the business is confirmed.

The Group ADR vs. Transient ADR Problem

The most common error in group displacement analysis is using ADR as the primary comparison. A group rate of $175 versus a transient ADR of $210 looks like a $35-per-room revenue loss. Apply that to a 150-room block and it appears to cost the hotel $5,250 per night in rate.

But that math ignores everything that doesn’t appear in the room revenue line. A group at $175 ADR with a $12,000 F&B minimum, 25% attrition protection, and 150 attendees generating two days of ancillary spend may produce substantially more total revenue than 150 transient rooms at $210 with no F&B attachment and normal transient ancillary capture rates.

Revenue managers who run displacement analysis using room rate alone are systematically undervaluing group business. This leads either to turning away profitable group in favor of transient that doesn’t materialize, or to approving group at rates that don’t compensate for the real displacement cost when transient demand is genuinely strong.

Both errors are avoidable with the right data. The problem is that the right data lives in the sales team’s deal record, not in the revenue management system.

What Accurate Group Contribution Analysis Requires

To evaluate group contribution to RevPAR and total revenue accurately, revenue managers need specific data points from each group opportunity, ideally before the proposal is finalized, not after the contract is signed.

- Contracted room block and rate: The baseline for room revenue calculation and displacement analysis

- F&B minimum spend: The contracted food and beverage minimum, which establishes a revenue floor beyond room revenue

- Meeting room or event space usage: Which spaces, for how many days, at what rental rate or as a comp against F&B minimum

- Attrition clause terms: What percentage of the room block must actualize, and what the revenue protection looks like if the group underperforms

- Estimated ancillary spend: Based on group profile, since corporate meetings versus leisure groups typically produce different ancillary capture rates

- Pickup history: For repeat groups, historical actualization data is the best predictor of real contribution versus contracted contribution

When the sales team captures this information consistently in a structured pipeline tool, revenue managers can run total value comparisons rather than ADR comparisons. The result is better displacement decisions, more accurate total revenue forecasts, and less friction between the sales and revenue management functions on pricing decisions.

For a structured look at how hotel group sales pipelines should be built to support this kind of data capture, see our guide to group-sales pipeline metrics.

Group Contribution and the Total Revenue Management Picture

RevPAR will remain the standard benchmarking metric for most ownership groups and asset managers. It’s simple, comparable, and widely understood. But internal revenue strategy decisions, particularly displacement analysis and group rate approval, should be made on a total revenue basis, not a room-revenue basis.

The hotels and management companies that consistently make better group decisions are the ones where revenue managers have access to deal-level data from the sales team before decisions need to be made. That requires a sales infrastructure that captures F&B estimates, attrition terms, and ancillary assumptions as a standard part of the pipeline record, not as a post-contract afterthought.

For a full look at how group sales and revenue management work together as a connected system, see our guide to where group sales meets revenue management.

Give Revenue Managers the Group Data They Need to Decide

Frequently Asked Questions

What is group contribution to RevPAR?

Group contribution to RevPAR refers to the portion of a hotel’s revenue per available room generated by the group segment. More broadly, group contribution to total hotel revenue includes room revenue, food and beverage, meeting room rental, and ancillary spend from group attendees. Evaluating group contribution only through room revenue understates the segment’s value for full-service hotels with significant event and F&B infrastructure.

Why is group ADR lower than transient ADR?

Group ADR is typically lower than transient ADR because groups are negotiated in advance at contracted rates, often in exchange for volume guarantees, committed F&B spend, and booking certainty. The lower room rate reflects the value the hotel receives in other forms: predictable occupancy, F&B revenue, and reduced distribution cost. A direct ADR comparison without accounting for total revenue contribution produces a misleading picture of group profitability.

How does group business affect hotel RevPAR?

Group business affects hotel RevPAR by contributing room nights at negotiated rates to the occupancy base. Strong group pace provides revenue managers with a firm occupancy foundation that supports higher transient pricing on remaining inventory. When group is behind pace, revenue managers may need to compensate by driving transient volume at more aggressive rates, which can compress overall RevPAR.

What is a displacement analysis in hotel revenue management?

A displacement analysis evaluates whether accepting a group booking at a negotiated rate generates more total revenue than the transient business it displaces. It compares total group value (rooms, F&B, event space, ancillary) against projected transient revenue for the same room nights on the same dates. An accurate displacement analysis requires deal-level data from the sales team, including F&B minimums, attrition terms, and group profile, before the group rate is approved.